Heretic Research 是专注于 Crypto 与 AI 交叉领域的独立研究机构。我们挖掘人声鼎沸之下的真实数据,并据此深度研究。我们独立于任何市场叙事。

An independent research house at the intersection of crypto and AI. We dig for the real data beneath the noise and build our research on it. We stand apart from any market narrative.

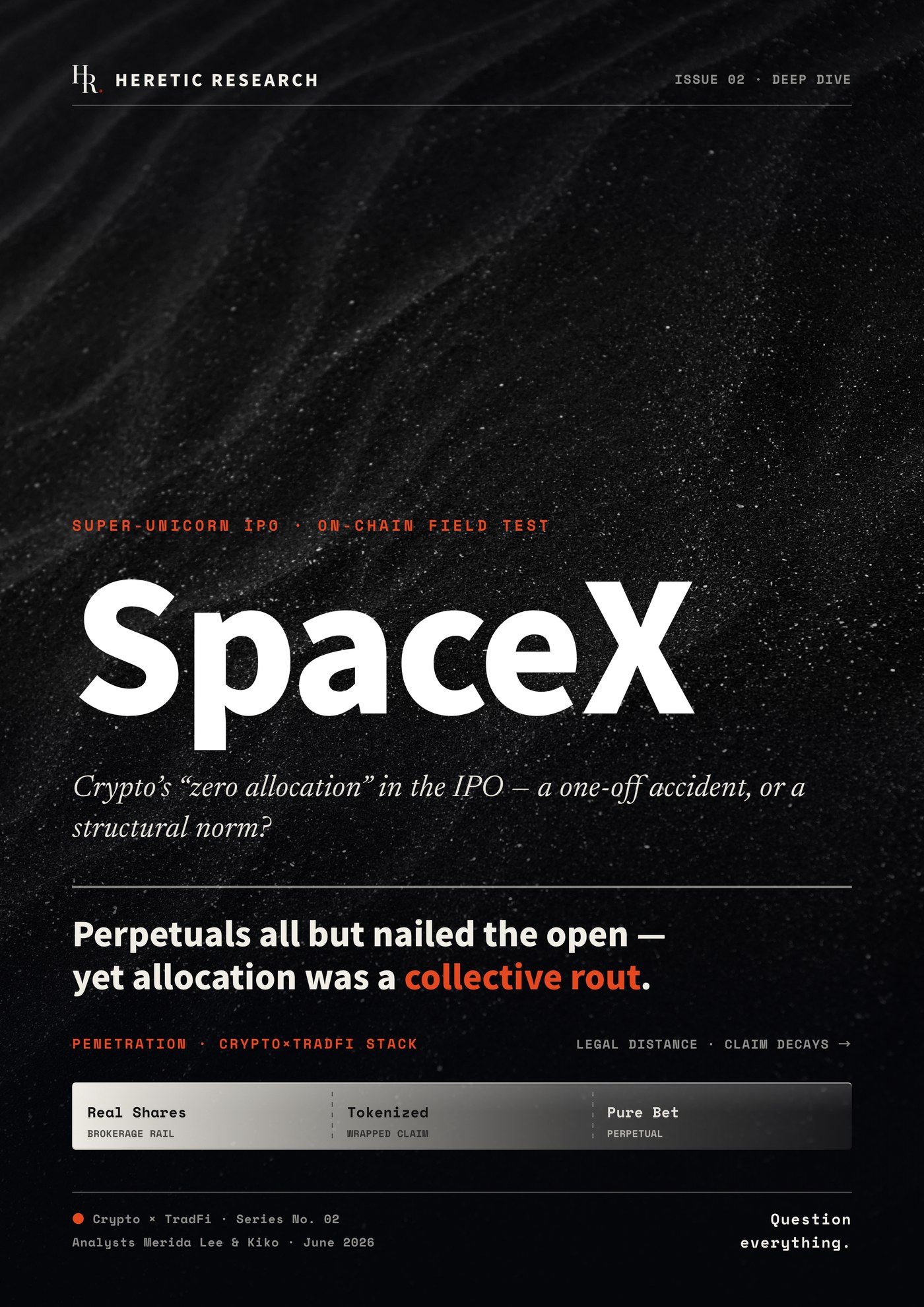

SpaceX listed on Nasdaq on June 12 — ~$75B raised, ~$2.1T valuation, the largest IPO in history. Crypto spun up at least four legal structures across five jurisdictions around one ticker, but they reduce to three layers: brokered real shares → tokenized wrappers → synthetic perpetuals, with rights decaying at each step.

On price discovery, crypto's penetration is real. Hyperliquid's pre-IPO perp volume jumped from under $5M to over $50M a day, and cross-venue VWAP now tracks close to the true open — the layer where riding the momentum pays off most fully.

On primary allocation, a collective rout. On listing day even Kraken — which holds an upstream sourcing agent — got only a token allocation; venues relying purely on it got nothing. The "zero allocation" wall is structural: the moat is a direct line into the underwriting syndicate for real supply; compliant wrapping is only a ticket to play.

The rebase episode exposed a second risk: you're not only trading SpaceX. A routine June 3 share-count increase (~10% dilution) drew three different rule responses from Binance, OKX and Hyperliquid; the arbitrage window opened between rule announcement and execution and closed within hours. The platform's corporate-action rules are themselves your exposure.

The whole game sits on an offshore architecture that excludes the US, UK, Canada and Australia — and the risk is deeply asymmetric. The upside is channel fees and retail flow; the downside can be zeroed by a single regulatory statement (PreStocks' Anthropic/OpenAI tokens once fell ~40%; 2021's equivalent stock tokens were shut down). Its fragility scales with its commercial success.